Featured

Table of Contents

If you're tackling a mountain of debt and could benefit from having a payment structure set up for you, this may be the best option for you. And, there are frequently charges and additional charges that may use depending on your situation and supplier.

Likewise worth keeping in mind financial obligation combination strategies do not always combine with other kinds of financial obligation accrual, such as buying a home or a brand-new car. The timing of when you sign up for a strategy can affect other financial decisions. Paying off any quantity of impressive credit card debt is a huge accomplishment and it is necessary to acknowledge the discipline it takes to arrive.

The alternatives provided here aren't the only choices you have for handling debt. Take a look at our list of methods to settle financial obligation for more choices.

Some 40 percent of U.S. adults stated paying down financial obligation is their largest anticipated expenditure in 2026, according to a recent study from the National Endowment for Financial Education. Financial obligation debt consolidation can assist debtors with a number of debt payments or high rate of interest integrate multiple balances into one and, in a lot of cases, lower the rate of interest on that debt."The right strategy ought to be based upon the stability of the customer's earnings, how quickly they require to pay off the debt and whether they need spending plan flexibility."The Independent talked to economists to determine three leading debt combination options: credit card balance transfers, individual loans and home equity loans.

Reviewing Interest Saving Tactics for Consumer Debt

How Nonprofit Programs Simplify Payments in 2026

Consumers dealing with debt can find a wide variety of financial obligation consolidation choices online. Finding the ideal one can offer long-lasting financial benefits (Getty Images)Credit card balance transfers often provide low- or no-interest financial obligation combination with a brief repayment timeline of typically up to 18 months, Baynes said. "You can discover many alternatives that provide 0 percent interest for 12 to 18 months, and they're best for those who have high-interest charge card balances," he said.

They generally have a transfer due date, constraints on the type of financial obligation you can move (credit card financial obligation is typically allowed) and charge a fee varying from 3 percent to 5 percent of the transferred balance. Considering that the average credit card limit was just $5,100 in the third quarter of 2025, according to the Federal Reserve Bank of Philadelphia, a balance transfer is ideal for consolidating smaller debts however can work for larger debts if a debtor's credit line permits.

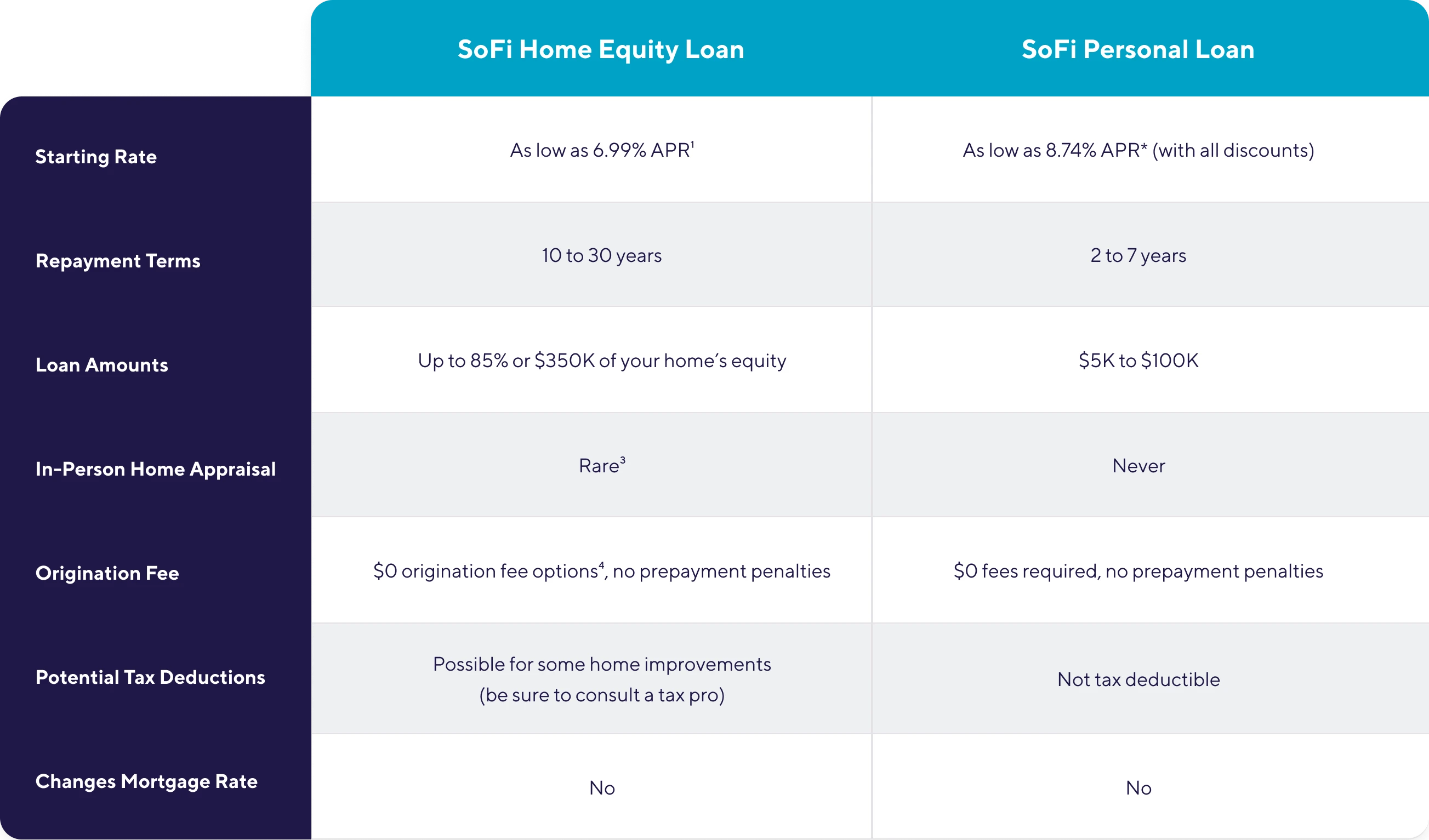

Personal loans provide a swelling amount of cash that can be used for almost any purpose, consisting of paying off financial obligations. Generally, personal loans have a fixed month-to-month payment, set repayment period and have lower rates of interest than credit cards, which is among their advantages. The typical interest rate on a two-year individual loan was 11.65 percent near the end of 2025, while the average credit card interest rate was 20.97 percent, according to the Federal Reserve's most current data.

Finding the ideal personal loan can be a cause for celebration due to the fact that their rates and payment terms can assist you pay down your credit card debt (Getty Images)Lenders set personal loan limitations that are more generous than those for most credit cards.

How Nonprofit Guidance Simplify Payments in 2026

Personal loans, on the other hand, have limitations of as much as $100,000, according to Credit Karma, if debtors have adequate earnings, a good credit rating and an appropriate debt-to-income ratio. Additionally, loan terms often vary from 12 to 60 months or longer, according to Rocket Loans, giving customers versatility for their benefit plan.

Be mindful that some lending institutions charge a charge for processing loan applications. Called "origination fees," they can be as high as 8 percent or 10 percent of the loan amount. Store around for lending institutions that waive this charge and offer competitive rates to maximize your cost savings. Home equity loans might be a great fit for homeowners with sufficient equity - the difference in between a home's value and its mortgage balance - and who need to combine a large amount of financial obligation.

Like an individual loan, a home equity loan generally offers predictable month-to-month payments with a fixed interest rate and repayment period. Nevertheless, term options are frequently up to 20 or thirty years, which can lower month-to-month payments. Home equity loans utilized for debt combination carry a considerable risk, stated accredited financial organizer Eric Croak, president of Ohio-based Croak Capital.

Reviewing Interest Saving Tactics for Consumer Debt"If you're consolidating credit cards with home equity, you much better believe you have the self-control of a Navy SEAL," Croak told The Independent in an e-mail. "You have actually simply protected your debt. Home equity loans offer fixed payments and competitive rates, but bring the threat of foreclosure if you can't keep up in repayment (Getty Images)Thinking about the high stakes and effect on a home's equity, Croak recommends using a home equity loan for financial obligation combination just under certain conditions.

2026 Reviews of Debt Management Programs

In addition to submitting comprehensive paperwork, customers may need to get a home appraisal and pay closing expenses of 3 percent to 6 percent of the loan amount, according to Rocket Mortgage.

A credit card consolidation loan lets you roll numerous high-interest credit card debts into a single loan with a set rate, term and one month-to-month payment. It might assist you conserve cash over the life of the loan with a competitive rate, putting you on a path to settling financial obligation.

Visit Equifax layer, Experian layer or TransUnion layer to acquire your credit report. Evaluation your credit report thoroughly and mark every thought mistake. If your credit report consists of incorrect info, get in touch with the credit reporting firm right away. They will examine your report, examine your claim, and make the correction if one is called for.

How Professional Guidance Simplify Debt in 2026

If the entry describes a debt, get in touch with the lender to work out payment alternatives. If there has actually been a disagreement, you can ask the credit reporting agency to include a note to your credit report explaining your side of the story. The bright side is that, as you enhance your habits, the majority of the unfavorable entries might eventually fall off your report with time.

{kind=link}

Latest Posts

A Comprehensive Review of Current Credit Relief

Using Loan Calculators for 2026

Critical Steps for Lowering Interest Payments Through Consolidation